INFORMATION

Industry News

Industry News

HOME > INFORMATION >

HOME > INFORMATION >

With 90% reliance on imports, how can China ensure that there is “copper” available in the face of a global copper resource gap?

2024-08-15

On June 13, CCTV reported that the price of copper futures traded on the London Metal Exchange has risen by more than 15% since the beginning of this year.

One of the important reasons for the high copper price is that the supply of copper metal cannot keep up with the current market demand. As the world's largest copper consumer, how can China ensure the stability and security of its supply chain?

Demand continues to release

Copper is widely used in light industry, construction, decoration, machinery manufacturing, aerospace, etc. due to its good electrical and thermal conductivity, soft and easy-to-process texture, strong wear resistance, and corrosion resistance. At the same time, copper is also an important industrial raw material and a trading variety in the global commodity futures market.

With the promotion of clean energy, the development and application of new energy vehicles, and AI, the consumption of copper metal is also increasing.

The latest report by the World Bureau of Metal Statistics shows that in January 2024 alone, the global consumption of refined copper will reach 2.4293 million tons. From January to May 2024, the apparent consumption of copper metal in China was about 5.893 million tons, a year-on-year increase of 5.8%. The apparent consumption in the first half of the year is estimated to be 7.133 million tons, a year-on-year increase of 2.3%.

Looking back at the data from the past two years, we can find that the consumption of copper metal has maintained an upward trend both worldwide and in China.

From 2021 to 2023, the global consumption of refined copper will be 25.26 million tons, 26.082 million tons, and 26.32 million tons respectively. Among them, China's copper metal consumption will be 13.88 million tons, 14.684 million tons, and 15.22 million tons respectively.

From the data, we can find that China's copper consumption accounts for half of the global copper consumption. Where is all this copper used?

As early as 2022, China's copper consumption accounted for 56% of the world's total, while the United States and the 15 EU countries accounted for 7% and 12% of the world's total copper consumption. In China, copper is used in electricity accounting for 46%, household appliances accounting for 14%, real estate accounting for 8%, transportation accounting for 12%, and machinery and electronics accounting for 9%.

By 2023, China's refined copper consumption is expected to reach 15.22 million tonnes, up 4.5% year-on-year; among them, the consumption of refined copper in the fields of electricity, home appliances, and mechanical electronics will account for 46.3%, 13.9%, and 8.3% respectively.

In addition, the growth of AI data center computing power has become a new driving force for the growth of copper consumption. At the GTC conference, NVIDIA released the GB200 chip architecture and the new NVL72 network architecture based on the architecture, which uses about 5,000 copper cables to connect switches and GPUs, highlighting the importance of high-speed copper cables in diversified high-speed transmission scenarios.

In fact, AI data centers’ demand for copper is not limited to power resources. Copper metal plays a key role in data center power distribution equipment, grounding, and interconnection. Everbright Securities Research Report predicts that by 2026, the amount of copper used in data centers will reach 710,000 tons, a 51% increase from 2023.

The production and sales of home appliances such as air conditioners and refrigerators have increased. Data shows that in April 2024, the monthly output of air conditioners was 30.33 million units, up 20% year-on-year; the output of refrigerators was 9.34 million units, up about 15% year-on-year, becoming the basic driving force for copper demand. Everbright Securities predicts that China's domestic demand for copper for home appliances will rise to 2.442 million tons in 2024, an increase of 8.6% year-on-year.

New energy facilities and equipment have also become major copper users. According to estimates, from 2024 to 2026, the global copper consumption for new energy vehicles will increase by 252,000 tons, 267,000 tons, and 235,000 tons, the copper consumption for new energy power generation will increase by 400,000 tons, 610,000 tons, and 310,000 tons, and the copper consumption for energy storage will increase by 55,000 tons, 70,000 tons and 45,000 tons.

In addition to new energy, home appliances, AI, and other fields, power grid investment will also boost the consumption of copper resources. Relevant estimates show that from 2024 to 2026, China's domestic copper demand will be 16.28 million tons, 16.66 million tons, and 28.76 million tons, up 0.9%, 2.3%, and 1.7% year-on-year.

As a major manufacturing country in the world, China's copper resource consumption accounts for half of the global consumption, but not all of this copper is used in China. A considerable portion of it has become commodities or commodity components and flows around the world.

The supply gap is still large.

Contradictory to the growing consumption of copper metal is the shortage of copper inventory and supply in the market.

Data from the London Metal Exchange shows that global copper inventories will be approximately 15.61 million short tons in 2022, about 6.69 million short tons in 2023, and only 2.66 million short tons in 2024, showing a continuous downward trend and at a historical low in the past decade.

The increase in consumption and the decrease in inventory have not only pushed up the market price of copper metal but also caused a gap in copper for production, affecting the stability and security of the copper supply chain.

According to statistics from the International Copper Research Group, global refined copper has been in short supply since 2018, and the global copper supply gap is 90,000 tons in 2023. It is estimated that from 2024 to 2026, the global copper supply will increase by 140,000 tons, 880,000 tons, and 580,000 tons respectively.

As the world's largest copper consumer, China's new energy vehicles, clean energy, and other industries have a high demand for copper, and it is expected that demand will increase by 330,000 tons, 920,000 tons, and 510,000 tons in the next three years. Taking various factors into consideration, the copper metal supply and demand gap in the next three years will be 280,000 tons, 310,000 tons, and 240,000 tons respectively.

What factors have combined to cause the supply and demand tension of copper resources?

First, the grade has dropped. According to statistics from ICSG, CRU, and Woodmac, the average grade of open-pit copper mines around the world has dropped from 0.81% in 1993 to about 0.6%; the average grade of underground mines has dropped from 1.36% in 1993 to 1.12%. By 2023, China's copper grade has dropped to about 0.56%.

Some people believe that the continued exploitation of existing mines has led to a continuous decline in copper grades.

Chile is the country with the richest copper reserves in the world, with about 190 million tons of copper reserves. However, as many copper mines age and copper ore grades decline, copper ore grades have dropped from 1% to 0.6-0.7% in the past 15 years. Some analysts believe that the decline in grade has prolonged mining time and increased investment costs for mining companies, leading to a reduction in the supply of copper resources in the market.

Second, investment is weak. As the market demand for copper resources increases, copper mine investment and construction are not optimistic, which has become a major problem for copper supply.

It is reported that, globally, existing mines and projects under construction can only meet 80% of market demand by 2030. Mining is a capital-intensive industry that requires long-term and large capital investment, generally 6 to 8 years, and some copper mines take 10 to 15 years from investment to output. The release of copper mine capacity lags significantly behind construction capital investment.

The capital investment from 2015 to 2017 basically corresponds to the copper mine capacity release cycle from 2023 to 2025. Except for the slow investment and construction due to the impact of the epidemic from 2020 to 2022, 2023 to 2025 will be a big year for copper mine production. After that, the growth rate of the copper supply will gradually slow down.

The problem is that many copper mines are underinvested and unable to meet and advance copper resource production. Some mining companies have cut production budgets due to shareholder dividends and used the money to pay dividends and repurchase shares.

In addition, environmental protection policies have imposed increasingly stringent restrictions on copper mining, increasing the difficulty and cost of mining production for mining companies. In addition, geopolitical risks are high, and some countries have even introduced copper export bans or production restrictions. The macroeconomic uncertainty brought about by many factors, as well as the long investment payback period of mining projects, has discouraged many mining investments. As a result, investment in the copper mining industry has been seriously insufficient in recent years, resulting in a reduction in the supply of copper resources.

While the market demand for copper continues to increase, the copper supply side is facing a possible contraction. Statistics show that by 2030, the global annual copper production may drop by 12% from 2021. By then, the annual copper production may remain at 19.1 million tons, and the supply gap may reach millions of tons.

Multiple measures to stabilize the supply chain

China is a world manufacturing powerhouse with a huge consumption of copper metal. From 2021 to 2023, China's copper metal consumption will be 13.88 million tons, 14.684 million tons and 15.22 million tons respectively. Copper, as one of the main raw materials for the production of finished products, flows to the world as goods and commodity components circulate domestically.

As a major copper consumer, my country is also a country with an extreme shortage of copper, and nearly 90% of its copper is imported from abroad. In addition, my country's copper ore has a poor grade and few rich ores, with an average grade of only 0.87%. Under the current situation of low concentration and poor grade of copper ore resources, mining small reserves is not as cost-effective as importing.

Considering the high dependence on imports, it is particularly important for my country to build a safe and stable global copper resource supply chain.

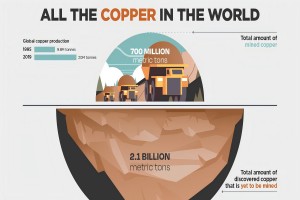

According to data from the United States Geological Survey, as of 2023, the world's proven copper reserves are 1 billion tons, mainly distributed in Chile, Australia, Peru, Russia, Congo, and other countries. The top five resource-rich countries control 57% of the world's copper resources. As a major copper-demanding country, my government has only 41 million tons of copper reserves, accounting for about 4% of the world's total.

In order to ensure the availability of copper, my country began its global layout decades ago.

China Minmetals, Aluminum Corporation of China, and Shougang Group have already established several large-scale mining projects in Peru and have obtained mining rights to several large copper mines there.

Another piece of good news is that the Aynak copper mine project, Afghanistan's largest, for which MCC and Jiangxi Copper acquired 100% of the operating rights for nearly US$3 billion in 2007, has been approved by the Afghan Ministry of Mines to continue operating.

It is understood that the Aynak Copper Mine is currently the second-largest undeveloped copper mine in the world, with a total resource of 705 million tons of ore and 10 million tons of copper metal.

In addition, Chinese companies also have mining rights to several high-grade copper mines in Australia, Zambia, Africa, Congo, and other countries.

In addition to overseas investment and cooperation in copper mine development, my country's domestic copper mine exploration has also achieved fruitful results. The "China Mineral Resources Report 2023" released by the Ministry of Natural Resources shows that in 2022, my country invested 657 million yuan in copper mine exploration, produced 1.874 million tons of copper concentrate, and proved copper reserves of 40.771 million tons.

At the same time, Chinese scientists have developed new application technologies for copper resources. For example, copper recycling technology can extract copper from a large number of scrapped equipment, and there is also "aluminum to copper" technology, which can make aluminum have the same performance as copper by treating aluminum accordingly. Through technological innovation and application, the source of copper metal can be greatly supplemented.

Economist Tan Haojun said that copper is an important strategic resource for China. We need to accurately analyze and predict the future trends of the copper market; cooperate with more copper-producing areas, rather than hanging the demand for copper on one or several companies to avoid being strangled by the other party; implement diversified imports of copper resources to ensure that there are no problems in the copper supply chain; moderately integrate resources overseas, increase investment in copper mine construction, and try to seize the initiative in the upstream resource market.

Tan Haojun said that by investing in overseas copper mining projects and owning equity, one will have the initiative, and even if the copper price rises, the negative impact on domestic companies will be relatively small; copper mine equity investment is actually a kind of interest balancing mechanism, otherwise, if the upstream resources are completely controlled by the other party, it will be inevitable that they will be strangled by the other party.

One of the important reasons for the high copper price is that the supply of copper metal cannot keep up with the current market demand. As the world's largest copper consumer, how can China ensure the stability and security of its supply chain?

Demand continues to release

Copper is widely used in light industry, construction, decoration, machinery manufacturing, aerospace, etc. due to its good electrical and thermal conductivity, soft and easy-to-process texture, strong wear resistance, and corrosion resistance. At the same time, copper is also an important industrial raw material and a trading variety in the global commodity futures market.

With the promotion of clean energy, the development and application of new energy vehicles, and AI, the consumption of copper metal is also increasing.

The latest report by the World Bureau of Metal Statistics shows that in January 2024 alone, the global consumption of refined copper will reach 2.4293 million tons. From January to May 2024, the apparent consumption of copper metal in China was about 5.893 million tons, a year-on-year increase of 5.8%. The apparent consumption in the first half of the year is estimated to be 7.133 million tons, a year-on-year increase of 2.3%.

Looking back at the data from the past two years, we can find that the consumption of copper metal has maintained an upward trend both worldwide and in China.

From 2021 to 2023, the global consumption of refined copper will be 25.26 million tons, 26.082 million tons, and 26.32 million tons respectively. Among them, China's copper metal consumption will be 13.88 million tons, 14.684 million tons, and 15.22 million tons respectively.

From the data, we can find that China's copper consumption accounts for half of the global copper consumption. Where is all this copper used?

As early as 2022, China's copper consumption accounted for 56% of the world's total, while the United States and the 15 EU countries accounted for 7% and 12% of the world's total copper consumption. In China, copper is used in electricity accounting for 46%, household appliances accounting for 14%, real estate accounting for 8%, transportation accounting for 12%, and machinery and electronics accounting for 9%.

By 2023, China's refined copper consumption is expected to reach 15.22 million tonnes, up 4.5% year-on-year; among them, the consumption of refined copper in the fields of electricity, home appliances, and mechanical electronics will account for 46.3%, 13.9%, and 8.3% respectively.

In addition, the growth of AI data center computing power has become a new driving force for the growth of copper consumption. At the GTC conference, NVIDIA released the GB200 chip architecture and the new NVL72 network architecture based on the architecture, which uses about 5,000 copper cables to connect switches and GPUs, highlighting the importance of high-speed copper cables in diversified high-speed transmission scenarios.

In fact, AI data centers’ demand for copper is not limited to power resources. Copper metal plays a key role in data center power distribution equipment, grounding, and interconnection. Everbright Securities Research Report predicts that by 2026, the amount of copper used in data centers will reach 710,000 tons, a 51% increase from 2023.

The production and sales of home appliances such as air conditioners and refrigerators have increased. Data shows that in April 2024, the monthly output of air conditioners was 30.33 million units, up 20% year-on-year; the output of refrigerators was 9.34 million units, up about 15% year-on-year, becoming the basic driving force for copper demand. Everbright Securities predicts that China's domestic demand for copper for home appliances will rise to 2.442 million tons in 2024, an increase of 8.6% year-on-year.

New energy facilities and equipment have also become major copper users. According to estimates, from 2024 to 2026, the global copper consumption for new energy vehicles will increase by 252,000 tons, 267,000 tons, and 235,000 tons, the copper consumption for new energy power generation will increase by 400,000 tons, 610,000 tons, and 310,000 tons, and the copper consumption for energy storage will increase by 55,000 tons, 70,000 tons and 45,000 tons.

In addition to new energy, home appliances, AI, and other fields, power grid investment will also boost the consumption of copper resources. Relevant estimates show that from 2024 to 2026, China's domestic copper demand will be 16.28 million tons, 16.66 million tons, and 28.76 million tons, up 0.9%, 2.3%, and 1.7% year-on-year.

As a major manufacturing country in the world, China's copper resource consumption accounts for half of the global consumption, but not all of this copper is used in China. A considerable portion of it has become commodities or commodity components and flows around the world.

The supply gap is still large.

Contradictory to the growing consumption of copper metal is the shortage of copper inventory and supply in the market.

Data from the London Metal Exchange shows that global copper inventories will be approximately 15.61 million short tons in 2022, about 6.69 million short tons in 2023, and only 2.66 million short tons in 2024, showing a continuous downward trend and at a historical low in the past decade.

The increase in consumption and the decrease in inventory have not only pushed up the market price of copper metal but also caused a gap in copper for production, affecting the stability and security of the copper supply chain.

According to statistics from the International Copper Research Group, global refined copper has been in short supply since 2018, and the global copper supply gap is 90,000 tons in 2023. It is estimated that from 2024 to 2026, the global copper supply will increase by 140,000 tons, 880,000 tons, and 580,000 tons respectively.

As the world's largest copper consumer, China's new energy vehicles, clean energy, and other industries have a high demand for copper, and it is expected that demand will increase by 330,000 tons, 920,000 tons, and 510,000 tons in the next three years. Taking various factors into consideration, the copper metal supply and demand gap in the next three years will be 280,000 tons, 310,000 tons, and 240,000 tons respectively.

What factors have combined to cause the supply and demand tension of copper resources?

First, the grade has dropped. According to statistics from ICSG, CRU, and Woodmac, the average grade of open-pit copper mines around the world has dropped from 0.81% in 1993 to about 0.6%; the average grade of underground mines has dropped from 1.36% in 1993 to 1.12%. By 2023, China's copper grade has dropped to about 0.56%.

Some people believe that the continued exploitation of existing mines has led to a continuous decline in copper grades.

Chile is the country with the richest copper reserves in the world, with about 190 million tons of copper reserves. However, as many copper mines age and copper ore grades decline, copper ore grades have dropped from 1% to 0.6-0.7% in the past 15 years. Some analysts believe that the decline in grade has prolonged mining time and increased investment costs for mining companies, leading to a reduction in the supply of copper resources in the market.

Second, investment is weak. As the market demand for copper resources increases, copper mine investment and construction are not optimistic, which has become a major problem for copper supply.

It is reported that, globally, existing mines and projects under construction can only meet 80% of market demand by 2030. Mining is a capital-intensive industry that requires long-term and large capital investment, generally 6 to 8 years, and some copper mines take 10 to 15 years from investment to output. The release of copper mine capacity lags significantly behind construction capital investment.

The capital investment from 2015 to 2017 basically corresponds to the copper mine capacity release cycle from 2023 to 2025. Except for the slow investment and construction due to the impact of the epidemic from 2020 to 2022, 2023 to 2025 will be a big year for copper mine production. After that, the growth rate of the copper supply will gradually slow down.

The problem is that many copper mines are underinvested and unable to meet and advance copper resource production. Some mining companies have cut production budgets due to shareholder dividends and used the money to pay dividends and repurchase shares.

In addition, environmental protection policies have imposed increasingly stringent restrictions on copper mining, increasing the difficulty and cost of mining production for mining companies. In addition, geopolitical risks are high, and some countries have even introduced copper export bans or production restrictions. The macroeconomic uncertainty brought about by many factors, as well as the long investment payback period of mining projects, has discouraged many mining investments. As a result, investment in the copper mining industry has been seriously insufficient in recent years, resulting in a reduction in the supply of copper resources.

While the market demand for copper continues to increase, the copper supply side is facing a possible contraction. Statistics show that by 2030, the global annual copper production may drop by 12% from 2021. By then, the annual copper production may remain at 19.1 million tons, and the supply gap may reach millions of tons.

|

|

|

Multiple measures to stabilize the supply chain

China is a world manufacturing powerhouse with a huge consumption of copper metal. From 2021 to 2023, China's copper metal consumption will be 13.88 million tons, 14.684 million tons and 15.22 million tons respectively. Copper, as one of the main raw materials for the production of finished products, flows to the world as goods and commodity components circulate domestically.

As a major copper consumer, my country is also a country with an extreme shortage of copper, and nearly 90% of its copper is imported from abroad. In addition, my country's copper ore has a poor grade and few rich ores, with an average grade of only 0.87%. Under the current situation of low concentration and poor grade of copper ore resources, mining small reserves is not as cost-effective as importing.

Considering the high dependence on imports, it is particularly important for my country to build a safe and stable global copper resource supply chain.

According to data from the United States Geological Survey, as of 2023, the world's proven copper reserves are 1 billion tons, mainly distributed in Chile, Australia, Peru, Russia, Congo, and other countries. The top five resource-rich countries control 57% of the world's copper resources. As a major copper-demanding country, my government has only 41 million tons of copper reserves, accounting for about 4% of the world's total.

In order to ensure the availability of copper, my country began its global layout decades ago.

China Minmetals, Aluminum Corporation of China, and Shougang Group have already established several large-scale mining projects in Peru and have obtained mining rights to several large copper mines there.

Another piece of good news is that the Aynak copper mine project, Afghanistan's largest, for which MCC and Jiangxi Copper acquired 100% of the operating rights for nearly US$3 billion in 2007, has been approved by the Afghan Ministry of Mines to continue operating.

It is understood that the Aynak Copper Mine is currently the second-largest undeveloped copper mine in the world, with a total resource of 705 million tons of ore and 10 million tons of copper metal.

In addition, Chinese companies also have mining rights to several high-grade copper mines in Australia, Zambia, Africa, Congo, and other countries.

In addition to overseas investment and cooperation in copper mine development, my country's domestic copper mine exploration has also achieved fruitful results. The "China Mineral Resources Report 2023" released by the Ministry of Natural Resources shows that in 2022, my country invested 657 million yuan in copper mine exploration, produced 1.874 million tons of copper concentrate, and proved copper reserves of 40.771 million tons.

At the same time, Chinese scientists have developed new application technologies for copper resources. For example, copper recycling technology can extract copper from a large number of scrapped equipment, and there is also "aluminum to copper" technology, which can make aluminum have the same performance as copper by treating aluminum accordingly. Through technological innovation and application, the source of copper metal can be greatly supplemented.

Economist Tan Haojun said that copper is an important strategic resource for China. We need to accurately analyze and predict the future trends of the copper market; cooperate with more copper-producing areas, rather than hanging the demand for copper on one or several companies to avoid being strangled by the other party; implement diversified imports of copper resources to ensure that there are no problems in the copper supply chain; moderately integrate resources overseas, increase investment in copper mine construction, and try to seize the initiative in the upstream resource market.

Tan Haojun said that by investing in overseas copper mining projects and owning equity, one will have the initiative, and even if the copper price rises, the negative impact on domestic companies will be relatively small; copper mine equity investment is actually a kind of interest balancing mechanism, otherwise, if the upstream resources are completely controlled by the other party, it will be inevitable that they will be strangled by the other party.